So far unseen Spreading Between Place and Futures Prices in Gold and Silver

Over the past few weeks, the financial markets have experienced an unprecedented expansion of spans between spot and futures prices for both gold and silver.

Traditionally narrow, these posts are expanded to as much as USD $ 60 for gold and over USD $ 1 for silver. This significant discrepancy has created unique arbitrage options, resulting in significant streams of physical metals from London to New York as dealers capitalize on lower spot prices in London and higher futures prices in New York.

From the time of writing, the spread is slightly narrowed with an USD 18,615 difference (0.65%) between spot gold (“gold”) and gold futures (“GC1!”). For silver, the spread at USD 0.745, corresponding to 2.27%.

Despite a clear arbitrage potential, these spans have not normalized as quickly as it would be expected of an effective market, suggesting underlying market failure in addition to simple arbitrage options.

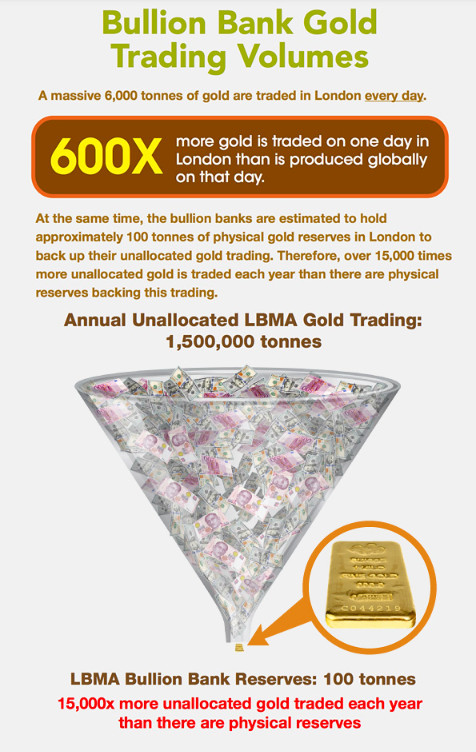

LBMA BULLION BANK CARTEL

The LBMA cartel for Bullion Banks has historically controlled the London OTC Psalm Prize for Gold, which operates within a system that prioritizes the interests of Bullion Banks over the actual physical gold and silver market. Opacity is the name of the game here.

LBMA lacks transparency and provides no public access to order book volumes or trading data. As a result, commercial practices remain hidden from control. In essence, so -called spot gold is treated more like a currency with little to no physical metal backing. In particular, LBMA itself has no gold reserves, instead of relying on its membership banks to maintain stocks.

Bullionstar has been a long time critic of LBMA, where we have repeatedly highlighted the lack of transparency, misleading data and prioritization of paper trade over physical gold. LBMA has for a long time incorrectly represented Vault Stock levels, creating a false sense of security about available metals.

Furthermore, LBMA enables the spread of unallocated synthetic paper gold, which allows gold banks to trade so-called gold and silver without actual physical support, which distorts real price discovery.

Controlled by gold banks, LBMA prioritizes their interests for individual savors and physical metal investorsThere favors financial institutions while undermining the integrity of the gold market.

See this Bullionstar Infographic at London Gold Market

Paper metal vs. physical metal

As many are aware of, there is a significant interruption between paper and physical gold and silver markets. Estimates suggest that for each ounce of physical metal, between 100 and 600 times more paper gold and silver are traded. Our infographic from 2021 estimates paper silver for physical silver at 243: 1. A recent analysis even places this ratio of 408: 1, which highlights the clean scale of this imbalance.

For years, LBMA and Comex have maintained the illusion that paper metal could be redeemed for physical metal. But with the United States, which is increasingly drawing physical supply from the market, the paper -based system is facing the mounting pressure. If only a small amount of paper metal holders start requiring physical delivery, the entire structure of the paper markets will collapse.

LBMA -Collusion ends

LBMA has historically been dependent on US financial institutions to help manage any problems. For gold liquidity, swaps and leasing arrangements have been used to prevent vaulting runs. However, the US institutions that now prioritize gold review and hamstring are prioritizing supporting international markets LBMA has lost a key backstop.

This shift leaves LBMA gold banks that are more vulnerable to physical deficiency, increase the counterparty risk and undermine confidence in non -allocated gold. Without US support, Bullion Bank’s resort to delaying settlements, expanding spreads or limiting redemptions – to further postpone the paper gold system.

Lbma is simply out of gold

London’s Gold Claring Banker – JP Morgan, HSBC, UBS and ICBC Standard – have exhausted their available physical gold for delivery and are now highly dependent on gold loans in the Bank of England. However, these borrowing options also occur exhausted.

As a result, these banks face a liquidity scare in their Loco London Gold Holdings, which increases the counterparty of LBMA gold banks, which deals with non -allocated “gold credit.” Inability to access adequate physical gold has led to paper gold requirements that deal with a discount, reflecting the growing difficulty in transforming them into actual metal.

See this Bullionstar infographic for information about Bullion Banking Mechanics.

“Gold is heavy” & lack of “guys with vans” and “Ocean of Silver”

LBMA has, as they always do, neglected this development and attributed to the high spreading and delivery delays to potential new tariffs rather than for structural problems or lack. They have stated that the 4-8 weeks of delay times for Gold Delivery from London vaults are due to logistical challenges.

LBMA A.Ppears have recently discovered that gold is heavy and that it needs “guys with vans”, ie. labor and transport resources to move gold. Maybe they never realized that gold was heavy when the vaults were empty anyway? But there is certainly no lack of supply if you have to rely on LBMA (Reuters on LBMA’s attitude). In terms of silver, LBMA claims that there is a sea of physical silver without any deficiency. However, the reality of Earth tells another story.

This is done all on the basis of highly elevated and sustained demand from Eastern countries, including China, India and Eastern European countries, which have quietly vaccumed all physical gold available but as a result of causing acute deficiency.

Convicted gold manipulators are running lbma

LBMA positions itself as the global authority of precious metals, but its actions suggest that it primarily serves the interests of its Bullion Bank members. While it claims to promote transparency, reporting is delayed, assembled and carefully controlled – to offer some real insight into the true state of the gold market.

Far from being an impartial regulator, LBMA is dominated by larger gold banks such as JP Morgan, who, despite being a convicted gold prize manipulator, continues to have an impact.

The appointment of JP Morgan’s former leader of precious metals, Michael Nowak, to the LBM board while under investigation of the market rigging exemplifies the association’s deeply rooted conflicts of interest. Instead of maintaining integrity, LBMA seems to act as a protective shield for the very institutions that distort and manipulate the gold market.

Bullionstar’s perspective on physical vs. paper markets

At Bullionstar, we observe that most market participants now continue to base their pricing on spot prices, albeit in some cases. If LBMA is exposed to being out of metal and ultimately defaulting – something we are already witnessing in a smaller form through delivery delays – we expect the price discovery to switch from London Spot to the Futures Market, provided Comex can facilitate actual physical deliveries rather than just stock recordings.

This remains uncertain. Comex is not designed for large physical retreats, as 99.96% or more of contracts are typically cash -boneding. Whether effortless physical metal can be extracted from Comex in significant quantities is uncertain.

Since market participants are aware that these markets are largely paper-based or semi-paper-based with minimal physical support, there may be a crib to ensure physical metal.

If this happens, the price of gold and silver will probably be determined by real physical markets. In such a scenario, it is reasonable to expect that the equilibrium price would be several times higher in view of the creepy relationship between paper metals and physical metals.

The trend is ready. Physical liquidity of real gold and silver is quickly drained from London and LBMA.

As a result, Singapore appears to be the world’s best jurisdiction to buy and store gold as a leading hub for wealthy savors and investors to keep their physical bullion stocks.

Price discovery changes from paper to physical markets

With London’s vaults running dry and coming, struggling to meet physical deliveries, the question arises: Who steps in to fill the void? The answer is that a major physical gold exchange has already emerged and builds significant infrastructure and trading in the last decade – Shanghai Gold Exchange (SGE). By 2024 alone, SGE saw an impressive 67.25% of traded gold, or 1,455 tonnes, delivered.

Since access to SGE is largely limited for non-Chinese units, there is a significant gap for a physical gold market in the West. This shift in the price discovery emphasizes the urgent need for more physically run markets outside China.